New York’s Inflation Refund Checks: A Closer Look at a Controversial Relief Program

The recent rollout of New York State’s inflation refund checks has sparked a lively debate among taxpayers, policymakers, and everyday residents alike. The program, designed to help mitigate the impact of increased sales taxes during times of heightened inflation, promises a one-time payment of up to $400 for eligible filers. However, as we take a closer look, there are several tricky parts and tangled issues that warrant a deeper discussion. In this editorial, we dive in to explore what exactly these checks mean, who benefits, and the hidden complexities behind their distribution.

Understanding the Purpose and Structure of the Check Program

The $2 billion initiative established by Gov. Kathy Hochul’s administration was intended as a form of direct repayment to taxpayers who, during times of rapid economic shifts, ended up bearing a heavier tax burden. With inflation driving a surge in sales tax revenue, state officials crafted this plan with the goal of returning some of that extra income back to the residents. The idea is straightforward: if you overpaid during a period of economic strain, you should receive some reimbursement.

Nonetheless, as we dig into the program, several off-putting details emerge. Prime among these is the fact that not every New York resident will receive a check. The eligibility criteria – which include filing a 2023 state tax return, meeting an income threshold, and not being claimed as a dependent on another return – inherently exclude many, especially Social Security beneficiaries who might not typically file a state return.

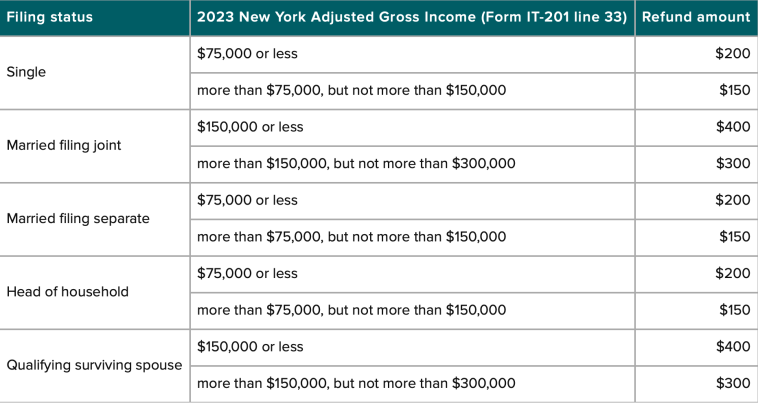

Accounting for Inflation: The Check’s Finances and Fairness

This refund check initiative is meant to compensate taxpayers for their extra sales tax payments during a period when inflation was particularly high. The basic premise rests on fairness: if prices spike and you unknowingly end up overpaying, you deserve some relief. However, the method to determine the actual payout and the accompanying guidelines reveal several confusing bits and complicated pieces.

For instance, the payout structure is scaled: a couple filing together, as well as a qualifying surviving spouse with an income below $150,000, can receive up to $400. In contrast, individuals filing by themselves or as the head of a household might receive as little as $150 if their annual income falls between $75,000 and $150,000. While this structured scale might be seen as a fair attempt to balance the relief across different income groups, the program’s overall fairness is under scrutiny by many critics.

Eligibility Criteria and the Social Security Conundrum

One of the most nerve-racking aspects of the program relates to the eligibility criteria. State officials have clarified that to receive an inflation refund check, residents must have filed their 2023 state tax returns. In turn, this disqualifies certain groups, particularly many Social Security and Supplemental Security Income (SSI) beneficiaries. These individuals, often those who rely on fixed incomes or have limited financial resources, might not need to file tax returns at all due to their modest incomes.

Tax professionals have pointed out several reasons why a Social Security recipient might choose not to file a tax return. These include scenarios such as the loss of a spouse who managed finances or a lack of mental capacity to engage with the taxing process. Without a filed return, the state finds it challenging to assess these individuals’ income levels against the income thresholds. In essence, some of the very people who need relief the most may be excluded by design.

Key Criteria for Eligibility

- Filing a 2023 state tax return

- Meeting established income thresholds

- Not being claimed as a dependent on another tax return

- Receipt of primarily Social Security or SSI benefits limits the chances of filing taxes

In summary, while the program’s intention is to offer relief, its reliance on tax filing as the primary measure of eligibility creates a catch-22 for many low-income elders and disabled individuals, setting off a cascade of bureaucratic challenges that leave significant numbers of residents on the sidelines.

The Ripple Effects on Small Business Owners and Industry Leaders

On the surface, the inflation refund checks are designed to serve individuals. However, the broader economic implications resonate throughout our varied industries—including small businesses, manufacturing, and even the emerging electric vehicles sector. When consumers receive a tax rebate, they are more likely to spend the extra cash, which can indirectly benefit local businesses. Yet, the uncertain distribution and its limited reach can also yield mixed signals.

For small business owners who have been painstakingly navigating the twists and turns of an ever-changing economic landscape, the refund checks represent both a potential boost in customer spending and an ongoing reminder of the nerve-racking economic policies. Many business leaders warn that although the boost in disposable income might offer temporary relief, the underlying problems of inflation and spending power will persist until substantive economic policy revisions are undertaken.

Compensation and Economic Impact: Evaluating the Trade-offs

When it comes to evaluating the emotional and financial trade-offs during periods of high inflation, the refund checks are a double-edged sword. On one hand, they offer a semblance of fairness by returning a portion of over-collected sales taxes – a move celebrated by many as an essential acknowledgment of the public’s financial hardship. On the other hand, the tangible benefit, in many cases, is limited, and its application appears to be riddled with confusing bits.

A number of industry experts have weighed in, questioning whether the chosen thresholds truly reflect the diverse economic circumstances faced by New Yorkers today. The program might be seen as a short-term fix rather than a super important, systemic change. The fact that almost two million of New York’s nearly 20 million residents might be left out of the relief program raises intense debate about equity and justice in policy design.

Eligibility Gaps: The Impact on Vulnerable Populations

One of the most immediate and tangible effects of the inflation refund check program is on vulnerable populations. Many Social Security and SSI beneficiaries will not receive these checks based solely on their non-filing status. This exclusion is particularly painful considering that many of these individuals are already grappling with the challenges of limited income and rising living costs.

While the state encourages even those who are not legally required to file to submit a tax return in order to claim certain credits and benefits, this recommendation fails to address the nerve-racking nature of the process for vulnerable individuals who may not have the support or resources required to complete their filings. The extra documentation, potential need for professional help, and the associated costs further complicate matters—adding layers of intimidating administrative hurdles.

Table: Comparison of Eligibility and Impact on Various Groups

| Group | Typical Eligibility Issues | Potential Exclusion Reasons |

|---|---|---|

| Low-Income Social Security Beneficiaries | Often do not file tax returns | Reliance solely on Social Security and/or SSI benefits |

| Working Families | May file returns but face income thresholds | Income above prescribed levels reduces check amount |

| Small Business Owners | Indirect beneficiaries through increased consumer spending | May not directly experience the refund check benefits |

| Disabled or Elderly Populations | Challenged by complicated filing requirements | Lack of support or resources to file |

This table clearly illustrates the uneven effects of the program, shining a light on the very real issues that can arise when a one-size-fits-all policy meets the nuanced economic realities of varied groups.

Tax Filing: A Necessary Hurdle or an Unfair Barrier?

It is worth taking a closer look at the decision to hinge eligibility on the filing of a 2023 state tax return. For many residents, filing taxes is a routine annual task. However, for a significant segment of New Yorkers—especially those on fixed incomes—the process is akin to steering through a maze of confusing bits. The lack of a requirement to file taxes for those with minimal income means that many residents simply do not participate in the process, thereby automatically excluding themselves from the refund check program.

Tax professionals emphasize that the decision not to file for many Social Security beneficiaries is not made lightly. Often, it is the result of considerable practical challenges. For instance, some individuals may no longer have someone to help manage their finances, or they may find the paperwork overwhelming. In these cases, the extra steps of filing to claim a public benefit can feel both intimidating and off-putting. Without the necessary support and resources, many of the underprivileged simply find it near impossible to meet the program requirements.

Evaluating the Administrative, Social, and Economic Implications

The rollout and implementation of the inflation refund checks offer a case study in the subtleties of public policy administration during turbulent times. Here are some of the small distinctions and fine shades that shape the public reaction:

- The administrative requirement to file a tax return is intended to ensure that checks are given only to those who have truly overpaid.

- The income thresholds are designed to balance the benefit, but set off a chain reaction where many with low or restricted incomes are inadvertently left out.

- The challenging nature of tax filing for certain groups complicates the policy’s application, as many eligible recipients simply fall through the cracks due to practical, off-putting obstacles.

- The program’s actual economic impact is dependent on how recipients spend the money, potentially boosting local economies and small businesses, though it is not a long-term fix.

Taken together, these factors underscore the delicate balancing act required in designing tax relief measures that are both fair and broad-based. The current inflation refund checks program is a super important experiment in this regard, aiming to mitigate the unintended consequences of inflation without overly burdening the state’s fiscal management.

Long-Term Perspectives: Is This a Band-Aid or a Systemic Solution?

While the refund checks provide an immediate, tangible benefit, critics argue that they might only serve as a temporary patch rather than addressing the nerve-racking underlying economic conditions. When inflation spikes and consumer prices soar, the quick fix of direct payments can offer welcome relief—but once the immediate crisis passes, the tough, tangled issues remain.

Policy experts suggest that long-term solutions need to focus on more sustainable economic reforms. These include strategies to improve wage growth, provide affordable housing, and restructure tax systems so that the burden doesn’t fall disproportionately on those least able to afford it. In other words, while refund checks might momentarily ease the pain, they do not address the full spectrum of challenges that inflation brings to our communities.

Practical Advice for Affected Taxpayers and Businesses

Amid the buzz and debate over the inflation refund checks, individuals and business owners alike are left pondering how best to secure their financial footing. If you fall into one of the groups that might be excluded from this program—such as relying solely on Social Security or SSI benefits—it is critical to explore every available option.

For taxpayers who are on the fence about filing a return solely to be eligible for the refund, consider the following steps:

- Reach out to free tax assistance programs like Volunteer Income Tax Assistance (VITA) or Tax Counseling for the Elderly (TCE) for help with the paperwork.

- Consult with a certified public accountant who can guide you through the process, particularly if your financial situation has recently changed due to personal or economic circumstances.

- Review your income and filing status carefully to verify your eligibility before investing time and possibly money into the filing process.

- Keep abreast of any additional state communications or revised guidelines in case the administration broadens the criteria or extends assistance to non-filers.

Business owners, on the other hand, should be aware that any increase in consumer spending driven by refund checks may be short-lived. It is a good opportunity to stabilize your operations by:

- Assessing your cash flow and ensuring that you have enough liquidity to manage through periods of economic uncertainty.

- Creating flexible marketing strategies that can accommodate shifts in consumer demand as a result of these one-time payments.

- Being prepared for potential delays in receiving checks by adjusting your short-term financial projections accordingly.

- Engaging with local business associations and chambers of commerce to lobby for more inclusive economic policies that support small business sustainability.

State Officials and Tax Experts: Their Take on the Program’s Mixed Success

State officials have highlighted that over 6.5 million of the estimated 8 million inflation refund checks have already been distributed. This number, however, masks the underlying issue: with a state population nearing 20 million, a significant segment of residents is left out of this relief as the checks target only those who meet very specific filing and income criteria.

Tax experts like David Silversmith and Carl Breedlove have warned about the potential pitfalls. As one CPA noted, if a beneficiary does not file a tax return, the state “has no way” to ascertain their true income or determine if they fall within the required income bracket. Consequently, the entire process becomes loaded with issues that are as much about administrative limitations as they are about economic fairness.

Another tax professional, Lisa Rispoli, commented that for many, the cost and effort required to secure an accountant’s assistance make the filing process feel overwhelming. For many in the affected demographic, the decision to file is not just about potential monetary gain—it is about weighing the super important benefits against a process perceived as intimidating and cumbersome.

Addressing the Confusing Bits: A Call for Policy Reforms

The debate surrounding the inflation refund check program is a perfect microcosm of the larger challenges facing modern fiscal policy. While the immediate need for relief is clear, the method chosen to deliver that relief is riddled with tense decisions and nerve-racking trade-offs. Instead of a one-off check, many suggest that the state should consider more holistic reforms, such as:

- Revising income thresholds to better capture the true economic hardships experienced by low-income and elderly residents.

- Simplifying filing processes, especially for populations that do not typically engage with complex tax systems.

- Expanding financial assistance programs to include educational outreach that demystifies the filing process for vulnerable groups.

- Developing a more inclusive fiscal strategy that combines refund checks with longer-term economic supports, such as housing subsidies or targeted wage enhancements.

These proposed reforms highlight a critical truth: while direct payments can lift the spirits and finances of many in the short run, real progress lies in addressing the tangled issues at the root of inflation and economic disparity.

Looking Ahead: Preparing for Future Economic Fluctuations

The current inflation refund check program, despite its many tangled issues, is a sign of evolving policy responses to an unpredictable economic environment. It is a reminder that policy must continuously adapt to the twists and turns of economic realities. As we continue to get into the details of fiscal policy and social welfare, future initiatives will benefit tremendously from the lessons learned in this round.

For state officials, the challenge now is two-fold. First, they need to ensure that the current program is as inclusive and efficient as possible. Second, they must begin planning for systemic reforms that can better withstand future inflation shocks. Here are a few forward-looking recommendations:

-

Enhance Digital Access:

Modernizing the filing process with more user-friendly digital platforms could help reduce the intimidating aspects for the elderly and low-income populations. Simple, accessible online filing tools backed by support centers can make a huge difference.

-

Community Outreach and Support:

Local governments and nonprofit organizations should team up to provide targeted assistance, educating residents on the benefits and procedures needed to access such relief programs. Workshops, helplines, and staffed community centers can help steer through the bureaucratic maze.

-

Reassessing Eligibility Guidelines:

A comprehensive review of income thresholds and filing requirements might reveal opportunities to include groups that are currently shuttered out of programs like this one. An inclusive approach could ensure that vulnerable populations receive the assistance they need.

-

Long-Term Fiscal Reforms:

Beyond one-off checks, the state may need to explore more robust frameworks that support sustainable economic growth. This includes strategies for wage enhancement, affordable healthcare, and housing initiatives that ultimately reduce the pain caused by inflation in the first place.

For business leaders and policymakers alike, these forward-looking actions are not just emergency measures but a blueprint for a more resilient economic future. They are a call to figure a path through the current maze of short-term fixes toward long-term, systemic solutions.

The Role of Communication and Transparency in Policy Implementation

Another essential theme that emerges from the analysis is the significance of clear communication by state agencies. The opaque nature of the eligibility criteria and distribution process has left many taxpayers puzzled and, at times, frustrated. Transparency in how decisions are made and how revenue surpluses are converted into taxpayer relief is not merely a technical requirement—it builds trust between the government and its constituents.

For residents and business owners alike, the need for clarity is paramount. Detailed local workshops and extensive FAQs on state websites can help clear up any remaining confusion. A more open dialogue about how these checks are calculated and distributed may also help in tempering expectations while guiding citizens through the necessary steps to receive their due benefits.

Lessons for the Future: What the Inflation Refund Check Program Teaches Us

While the inflation refund check initiative is still in its early stages, there are several key takeaways that can inform future economic relief measures. These include:

-

Inclusivity Matters:

Any program that aims to be truly beneficial must account for the diverse financial realities of its target population. Policymakers should strive to ensure that vulnerable groups—especially low-income and elderly residents—are not inadvertently sidelined by administrative requirements.

-

Simplicity is Key:

By reducing the intimidating and complicated pieces of the filing process, the state can help ensure that more residents are able to take advantage of any available benefits. Simplified guidelines, paired with free assistance programs, can go a long way in this regard.

-

Holistic Policy Approaches:

Short-term relief is necessary during economic crises, but long-term solutions require addressing the hidden, tangled issues that underlie economic distress. A mix of immediate financial support and comprehensive economic reforms is essential for creating a resilient fiscal framework.

-

Effective Communication and Transparency:

Policymakers must proactively communicate each step of the process and be transparent about the criteria and limitations of the program. Doing so will not only demystify the process for many but also establish a stronger foundation of trust between citizens and government agencies.

These lessons are a valuable resource as we continue to tackle issues related to inflation and economic security. The goal is not simply to provide a temporary financial band-aid but to foster long-term reforms that truly lift up every segment of our community.

Conclusion: Balancing Short-Term Relief with Long-Term Goals

The New York State inflation refund check program stands as a testament to the challenges of managing economic crises through rapid policy responses. While its primary goal—to return some of the overpaid sales tax revenue to residents—resonates as a gesture of fairness, the implementation reveals many of the subtle details and hidden complexities that make such relief programs both essential and deeply problematic.

This editorial has taken a closer look at the program’s foundations, its varied impact on different groups, and the logistical as well as administrative hurdles that continue to plague its success. Whether you are an individual taxpayer grappling with an intimidating tax filing process or a small business owner trying to predict consumer behavior, understanding these elements is crucial for making informed decisions in today’s loaded economic landscape.

Ultimately, as New York State residents and as a community, we are called upon to engage in conversations about refinement and reform. The inflation refund check program, with all its merits and limitations, should serve as a stepping-stone toward better, more inclusive policies that address not only the immediate pain of inflation but also the underlying structural challenges that contribute to financial instability.

By adopting clearer, simpler, and more inclusive approaches, policymakers can transform short-term relief measures into super important, long-lasting benefits that truly support every segment of society. In doing so, we take a significant step toward building an economic future where the twists and turns of inflation are met with robust, sustainable, and fair solutions.

As we continue to figure a path through these challenging times, the conversation must shift from mere temporary fixes to the development of comprehensive reforms. These reforms should ensure that every taxpayer, whether reliant on Social Security benefits or running a local business, has the chance to secure financial stability without having to navigate a maze of intimidating bureaucracy.

New York’s inflation refund checks are a starting point—a signal that even amid economic turbulence, there is a willingness to acknowledge past overpayments and attempt to restore balance. However, for this program to serve as a true catalyst for broader economic reform, it must evolve. This evolution requires addressing not just the off-putting administrative details, but also the systemic issues that lie at the heart of our economic challenges.

In our collective pursuit of an equitable society, the dialogue around these refund checks should ultimately spark a broader conversation about fairness, inclusivity, and sustainable economic policy. Only by working together and embracing both immediate relief and long-term solutions can we ensure that all New Yorkers are equipped to thrive in an ever-changing economic landscape.

Originally Post From https://www.newsday.com/news/region-state/new-york-state-inflation-reduction-check-tax-returns-xutvn8vr

Read more about this topic at

Inflation refund checks – Tax.NY.gov

$400 Inflation Refund Check for November 2025, Who …