IRS Unveils Higher Capital Gains Tax Brackets for 2026: A Closer Look

The Internal Revenue Service’s recent announcement of higher capital gains tax brackets for 2026 has stirred a mix of reactions among investors, small business owners, and financial advisors. This editorial takes a closer look at the update, unpacking the tricky parts of calculating taxable income, the tangled issues surrounding the new brackets, and the broader implications for different stakeholders. We will dig into the fine points of these changes, all while comparing them to other tax adjustments set to kick in next year.

In the wake of other updates—including higher federal income tax brackets and an increased estate and gift tax exemption—the modifications to the capital gains brackets are especially noteworthy. For many, these changes have come as a surprise, particularly given the backdrop of uncertainty caused by a government shutdown that led to the furlough of nearly half of the IRS workforce.

Understanding Taxable Income Changes and Capital Gains Rates

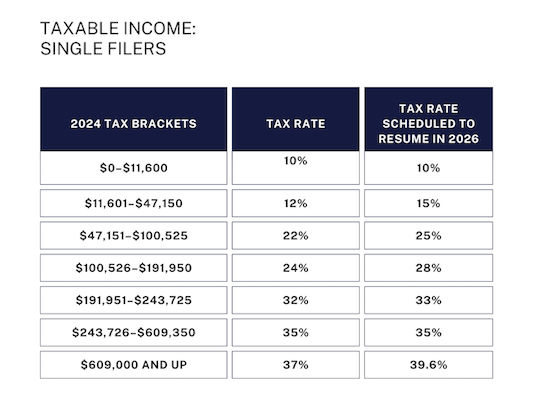

Determining the taxable income you report involves subtracting either your standard or itemized deductions from your adjusted gross income. For 2026, the standard deduction has been set to $16,100 for single filers and $32,200 for married couples filing jointly. This means that a single filer reaching a taxable income of $49,450 or less will qualify for the 0% long-term capital gains rate, while a married couple filing jointly can earn up to $98,900 and still pay no long-term capital gains tax.

These new thresholds are not just arbitrary numbers. They represent a recalibration of the IRS’s approach to taxing investments held for longer than one year. While some might view these adjustments as designed to ease the tax burden on investors, others believe they could lead to a reallocation of assets and adjustments in retirement planning strategies.

It is important to note how these seemingly small changes in taxable income thresholds can have little twists on investment behaviors, particularly among those managing both retirements and small business ventures.

Capital Gains Tax Brackets 2026 Update for Investors

Investors who plan on holding assets for longer than a year have reason to pay attention to these modifications. The new brackets suggest that many might soon find themselves needing to figure a path through the revised IRS structure. Here, we discuss what this means practically:

- Easing the Burden for Some: With higher thresholds for the 0% capital gains rate, investors might enjoy a temporary reprieve, especially those in lower taxable income brackets.

- Shifting Investment Strategies: Some investors may become more willing to hold on to assets longer, for fear that selling at an inopportune moment might push them into a higher tax bracket.

- Incentives for Longevity in the Market: The adjustments are seen as a push toward sustainable, long-term investment behavior, an approach that benefits overall market stability.

However, the fine shades of these changes reveal that investors must also consider the nerve-racking idea of potential future adjustments. The IRS’s decision to modify taxable income limits and other tax provisions may signal further changes on the horizon. As such, constant vigilance and regular updates from trusted financial advisors become essential.

Impact on Small Business Owners and Entrepreneurs

Small business owners are particularly sensitive to shifts in tax policy as these updates may directly affect their overall tax liability. Many entrepreneurs rely on a mix of personal and business income, making unexpected changes in either tax brackets or deductions a matter of intense focus.

When the IRS increased figures across numerous provisions—from federal income tax brackets to earned income tax credits—small business owners needed to work through the problem of adjusting their financial planning to account for these new thresholds. Changes like these can appear overwhelming at first glance, but a systematic review of one’s finances may reveal areas where adjustments are possible, and even beneficial.

For instance, consider the following table summarizing key changes for small business owners:

| Provision | 2025 Value | 2026 Update | Potential Impact |

|---|---|---|---|

| Standard Deduction (Single) | ~$13,850 | $16,100 | Reduces taxable income |

| Standard Deduction (Married Filing Jointly) | ~$27,700 | $32,200 | Minimizes tax burden |

| 0% Capital Gains Threshold (Single) | Lower Benchmark | $49,450 | Encourages holding assets longer |

| 0% Capital Gains Threshold (Married Filing Jointly) | Lower Benchmark | $98,900 | Favors joint investment strategies |

The table above provides a clear breakdown for business owners, illustrating how these adjustments can lower overall tax liability if leveraged correctly. Yet, the fine details of each provision require careful planning and, in many cases, consultation with financial or tax professionals.

Retirement Planning: A Closer Look at the IRS Update on Capital Gains

For retirees and those nearing retirement, the new capital gains brackets are super important. Investments in stocks, bonds, and mutual funds often make up a significant portion of retirement portfolios. Thus, understanding these thresholds can make a real difference in long-term planning.

One of the subtle parts of the update is its potential impact on retirement withdrawal strategies. Let’s break down some of the key considerations:

- Income Timing: Retirees might plan the sale of profitable assets during years when their income remains below the 0% threshold, ensuring they maximize tax advantages.

- Asset Reallocation: With the increased limits in place, rebalancing portfolios might become less nerve-racking, as investors can hold onto high-yield assets for longer and wait for optimal tax circumstances.

- Planning Ahead: Working closely with tax advisors to forecast income and manage deductions is essential, especially when considering that taxable income encompasses both earned and investment income.

These measures allow retirees to figure a path through the complicated pieces of retirement planning and ease the overall cost of exiting high-tax brackets too quickly. With the 0% long-term capital gains rate accessible at higher income levels, there is an incentive for a more gradual, sustained conversion of taxable assets.

How Increased Standard Deductions Alter Tax Strategies

The increment in standard deductions for both single filers and married couples filing jointly is one of the more approachable aspects of the 2026 IRS update. While some individuals might see this as merely a small numerical change, the reality is that it can have a significant impact on overall tax planning.

An increase in the standard deduction reduces the taxable income right from the start. For many, this acts as an immediate relief, allowing for a larger margin before confronting higher tax brackets. Here are several perspectives on how these changes might play out:

- Greater Disposable Income: With a higher standard deduction, individuals might notice a temporary increase in their take-home income, which can be reinvested or redirected toward other financial goals.

- Simplified Financial Planning: Not having to itemize deductions every year can simplify the process, especially for those not facing many complex or tricky parts in their finances.

- Unified Approach for Various Taxpayers: Whether one is an investor or a small business owner, a higher standard deduction offers a common ground for reducing taxable income.

In reality, the standard deduction acts as a shield against the overall tax burden; yet, one must consistently work through the subtle parts of tax planning to ensure that these benefits are maximized each year.

IRS Adjustments Amid Government Shutdown Concerns

Adding another layer of complexity, the IRS report on higher capital gains tax brackets was released just days after the agency announced a furlough affecting nearly half of its workforce due to a government shutdown. This has led many observers to wonder about the practical and immediate consequences of having a reduced workforce managing such essential updates.

Several aspects are on edge when considering this situation:

- Public Confidence: The simultaneous release of tax updates during a government shutdown can feel overwhelming, leaving taxpayers to cope with both administrative delays and sudden policy shifts.

- Implementation Timelines: With key personnel furloughed, there might be delays in customer service and support, making it harder for taxpayers to get timely answers on how to adjust their financial plans.

- Long-Term Impact: The government shutdown itself may lead to further adjustments in spending, policy implementation, and even revisions to tax law adjustments as unforeseen complications arise.

The interconnected issues of personnel shortages and updated tax law mean that investors, entrepreneurs, and retirees alike need to take a proactive stance. It might require extra effort and, in some cases, the counsel of trusted professionals to manage your way through these challenging times.

Planning for the Future: How to Figure a Path Through the New Tax Landscape

One of the chief concerns among financial professionals is how to effectively work through the various pieces of tax legislation while ensuring that personal and business finances remain robust. The new capital gains tax brackets do not operate in isolation; they interact with a host of other tax provisions and future revisions. Here are some clear steps to guide you through this evolving landscape:

- Review Your Investment Strategies: Consider the timing of sales. By understanding the new thresholds, you can plan asset sales for years when your taxable income falls within the 0% capital gains bracket.

- Optimize Your Deduction Claims: With higher standard deductions, evaluate whether itemizing in previous years still makes sense, or if standard deductions now offer a simpler and more beneficial route.

- Consult With Financial Experts: The subtle details of these tax changes—like slight differences in taxable income calculations—are best handled with the assistance of seasoned tax professionals or financial advisors.

- Plan for Future Updates: Recognize that tax laws are never static. Regularly revisiting and revising your tax strategy is essential when facing a landscape that is full of problems and loaded with potential policy shifts.

By taking the time to dig into the new IRS guidelines and manage your way through the related changes, you can ensure that your financial strategies remain resilient and adaptable. The key is to prepare well in advance and stay informed about the evolving regulatory environment.

Delving Deeper Into the Fine Details of Capital Gains and Tax Planning

When it comes to deeper tax planning, it’s not just about knowing the numbers but understanding how they interact with your overall financial picture. Let’s take a closer look at some of the subtle parts that often get overlooked:

- Understanding the Calculation: Taxable income is calculated by subtracting the greater of the standard or itemized deductions from your adjusted gross income (AGI). Even small changes in any of these variables can shift you into a different tax bracket.

- Capital Gains Versus Ordinary Income: Recognize the difference between income derived from long-term investments and ordinary wages. The IRS treats these two differently, which is crucial when planning your year-end income.

- Long-Term vs. Short-Term Gains: Investments held for over a year qualify for long-term capital gains treatment. This status not only benefits from lower tax rates but also demands careful consideration in timing your asset disposition.

Mapping out these finer details can sometimes feel like steering through a maze of confusing bits and nerve-racking paperwork. However, by breaking down the process into manageable steps, individuals and business owners alike can better face the twists and turns of tax season.

Advice for Financial Advisors and Tax Professionals

For those who work directly with clients, these IRS updates present both an opportunity and a challenge. On one hand, this is a chance to educate clients on the new tax landscape; on the other, it means preparing them for a period of adjustment rife with small distinctions and subtle details.

Here are several tips to help advisors guide their clients through these revisions:

- Stay Updated: Regularly review IRS announcements and policy updates. Being proactive helps you steer through the changes ahead of time.

- Develop Clear Communication Strategies: Use tables, bullet lists, and visual aids to help clients understand complex concepts. Breaking down the fine points into digestible pieces can ease the intimidating nature of tax law.

- Offer Scenario Analyses: Present multiple scenarios with varying income levels to demonstrate how switching from one capital gains bracket to another can affect overall tax liability.

- Build Future-Proof Plans: Encourage clients to plan for future changes. Tax laws today might be modified further in the coming years; having a flexible strategy can be a must-have defensive tactic.

By working closely with their clients and continuously updating their knowledge base, financial advisors and tax professionals can help demystify the process. This collaborative approach not only builds trust but also prepares individuals to handle the unpredictable aspects of tax law modifications.

Exploring the Broader Economic Context

The IRS update on capital gains tax brackets does not exist in a vacuum. It is intertwined with broader economic trends and policy decisions that have significant impacts on national and global markets. The current administration’s fiscal policies, combined with ongoing government shutdown concerns, create a backdrop that is both full of problems and rife with potential opportunities.

Let’s break down how these broader economic factors might influence the new IRS guidelines:

- Government Spending and Policy Priorities: With shifts in workforce availability at the IRS, public perception and trust in government efficiency have taken a hit. This tension might lead to future adjustments in tax policies as lawmakers attempt to balance revenue needs with public opinion.

- Market Stability Concerns: Changes in capital gains tax brackets play a subtle role in market behavior. Investors often factor in these tax changes while making decisions, potentially leading to shifts in asset allocation or investment timing.

- Small Business Vulnerability: In an already complex economic environment, small businesses may face added challenges. They need to remain agile, recalibrate their financial models, and, when necessary, consult with experts to ensure compliance and advantage.

Understanding these broader issues is critical for anyone trying to piece together the full impact of the IRS announcement. The interplay between economic trends and tax policies suggests that while the changes may initially offer relief to some, they may also spark further regulatory and fiscal adjustments down the line.

Key Takeaways on the New Capital Gains Brackets

In summary, the IRS’s decision to raise capital gains tax brackets for 2026 should be seen as a multifaceted update with far-reaching consequences for investors, business owners, and retirees alike. Below is a concise recap of the most important points:

- Higher Thresholds: The new limits of $49,450 for single filers and $98,900 for married couples filing jointly ensure that many taxpayers can achieve a 0% long-term capital gains rate, provided their taxable income remains within these bounds.

- Impact on Investment Decisions: Investors may adjust their strategies, choosing to hold assets longer to benefit from the tax advantage.

- Special Consideration for Retirees: Retirees now have an added incentive to manage asset sales carefully to prevent an unexpected tax burden—an essential adjustment to their withdrawal strategies.

- Effect on Small Business Owners: Changes in standard deductions and taxable income calculations mean that entrepreneurs must be more scrupulous in reviewing and updating their financial plans.

- Economic Implications: These tax updates, set against the backdrop of government shutdown concerns and broader fiscal policies, underscore the need for ongoing vigilance and strategic planning.

This summary emphasizes that while the updated brackets provide some immediate benefits, they also come with a host of challenges that necessitate careful deliberation and future-proof financial planning.

Looking Ahead: What to Expect in the Coming Years

In a landscape peppered with ongoing government shutdowns, workforce challenges, and constant policy shifts, taxpayers have every reason to remain alert. While the current adjustments present opportunities—particularly for those who plan ahead—they also carry an element of unpredictability. As federal tax policy continues to evolve, investors, entrepreneurs, and retirees should anticipate additional revisions and allocate time to reassess their tax plans frequently.

In the near future, it would not be surprising to see further tweaks in areas such as:

- Federal Income Tax Brackets: As the IRS adjusts other tax codes, more changes in income tax brackets could follow.

- Estate and Gift Tax Exemptions: With continued attention on shifting wealth demographics, expect potential modifications to estate planning strategies.

- Earned Income Tax Credit and Other Deductions: As these changes are integrated, other credits may be recalibrated to reflect broader economic conditions.

This forward-looking approach promotes a mindset of continuous review—essential for anyone looking to safeguard their financial future amidst evolving tax policies. It may be wise to periodically dive in and examine your financial portfolio with respect to these updates, ensuring that you are always one step ahead in your tax planning efforts.

Conclusion: Embracing Change in an Evolving Tax Environment

The announcement of higher capital gains tax brackets for 2026 is more than just an isolated tax update—it signifies a major shift in how investors and small business owners might plan for the future. With increased thresholds, the update offers a reprieve for those in lower taxable income brackets, yet it also demands that all affected parties take a closer look at their overall financial strategies.

Whether you are an investor eyeing long-term asset growth, a small business owner trying to maximize every dollar of your taxable income, or a retiree hunting for ways to stretch your savings, these tax changes underscore the importance of regular financial check-ups and staying informed about the fine details of tax legislation.

While the challenges may seem overwhelming at times, the key lies in breaking down the confusing bits into manageable actions—leveraging updated deductions, planning asset sales around favorable tax thresholds, and collaborating with financial professionals to adapt as necessary. In short, the IRS update provides an opportunity to both refine your current strategy and prepare for future twists and turns in the tax landscape.

As we look ahead to 2026 and beyond, it is essential that tax planning remains a dynamic, proactive process. With careful analysis and strategic adjustments, taxpayers can not only cope with these changes but also harness them for long-term financial benefit. In a time of government uncertainties and shifting policy priorities, being well-prepared and informed is, without a doubt, a must-have trait for securing your financial well-being.

Ultimately, these modifications are a reminder that tax policies are ever-changing. They invite us all to take a closer look at not only the figures in our annual tax returns but also the broader economic context that shapes our financial decisions. By steering through these adjustments with both caution and confidence, you can ensure that the path forward in this evolving tax environment remains both manageable and promising.

Originally Post From https://www.cnbc.com/2025/10/09/capital-gains-tax-2026-federal.html

Read more about this topic at

The IRS upped capital gains brackets: How much you can …

IRS unveils higher capital gains tax brackets for 2026